|

City of Calgary, February 1, 2021 – January sales were the highest they have been for the month since 2014, as housing market momentum from the end of 2020 carried over into the start of 2021. Sales activity improved across all product types and across all price ranges. “Discount lending rates are exceptionally low, which is likely attracting all types of buyers back into the market,” said CREB® chief economist Ann-Marie Lurie. “New listings in the market were also slightly higher than what was available over the past two months, which is providing more options to purchasers.” January’s new listings were 2,246 relative to the 1,208 sales in the market, causing inventories to edge up over December levels. These types of movements are typical for January, but 2021 is starting the year with 4,035 units in inventory. This is far lower than the past six years. Benchmark prices remained at levels relatively consistent with prices recorded at the end of 2020, but they reflect a year-over-year gain just below two per cent. Average and median prices recorded higher year-over-year gains, likely due to larger gains in sales in the higher end of the market. Those segments do not have the same inventory constraints as lower-priced product. HOUSING MARKET FACTS Detached January sales activity improved across most prices ranges. However, limited inventories for homes priced below $500,000 ensured conditions in those segments remained firmly in sellers’ market territory. This likely prevented stronger sales improvements in this portion of the market. However, with better supply options at the upper end of the market, sales activity improved. The citywide months of supply was just over two months, a significant drop from last January where levels were nearly five months. The tighter conditions in this segment supported further gains in prices, which currently sit nearly three per cent above last year’s levels. Year-over-year price gains range significantly throughout the districts of the city. The largest gains occurred in the North and South East districts. Prices remained relatively unchanged over the previous year in the City Centre and West districts. Semi-Detached January sales activity rose over last year’s levels due to gains across most districts. The West end district continues to see slower activity than the previous year. New listings improved from December levels. This is causing some monthly gains in inventories, but inventory remains well below levels seen last year and the months of supply remained below three months. Price activity did vary depending on location. Year over year, prices remain over one per cent higher than last year’s levels thanks to strong gains in the North and South East districts. However, persistently high levels of inventory compared to sales contributed to the significant price decline occurring in the West district. Row Thanks to gains across nearly every district, sales activity improved compared to the previous year. Unlike the detached and semi-detached sectors, row new listings trended up relative to last month and levels recorded last year. The rise did result in some monthly gains in inventory levels and caused the months of supply to rise to nearly five months. This is not entirely unusual activity for January. The months of supply remains well below last year’s levels at nearly seven months. Citywide row pricing remained relatively stable compared to last year and last month. However, there was significant variation depending on location. Year-over-year price gains exceeded four per cent in the City Centre, West and East districts. Meanwhile, prices eased by over three per cent in the North and South East districts. Apartment Condominium For the third month in a row, apartment condominium sales rose above levels recorded in the previous year. January levels are the best we have seen since 2014. While new listings have eased compared to last year, they recorded a significant jump over December levels, keeping inventories elevated relative to sales activity. While prices remain well below previous highs, there were some districts that recorded year-over-year gains. The strongest gains occurred in the North East, East and South districts. However, prices continue to fall in the City Centre, West and South East districts. REGIONAL MARKET FACTS Airdrie Sales activity stayed strong in January. With 103 sales, this was the best January since 2007. New listings improved compared to last month, resulting in some monthly gains in inventory levels. However, the months of supply has remained relatively tight. With conditions continuing to favour the seller, benchmark prices trended up relative to last month. At $349,100, benchmark prices are over five per cent higher than levels recorded last January. The strongest year-over-year price gains occurred in the detached and semi-detached sectors. Cochrane Cochrane sales improved from last January’s levels, but we also saw a notable rise in new listings. This caused the sales-to-new-listings ratio to ease to 63 per cent. This is a significant improvement over last month, which saw sales levels exceed the level of new listings in the market. Overall, conditions remain relatively tight, with the months of supply staying below three months. Benchmark prices recorded year-over-year gains across all property types. Overall, benchmark prices remained over four per cent higher than last January’s levels. Okotoks After several months of relatively weak new listings, January saw some pickup in new listings relative to the last quarter of 2020. Sales remained relatively consistent with last year’s levels, causing the months of supply to trend up to three months. This is higher than the extremely tight levels seen at the end of 2020, but it is still significantly lower than the six-plus months recorded in January of last year. Benchmark prices remained stable compared to last month, but they are over three per cent higher than last January. The gains were driven by the detached sector, as prices continue to ease in the semi-detached, row and apartment sectors. Provided by CREB City of Calgary, January 4, 2021 –

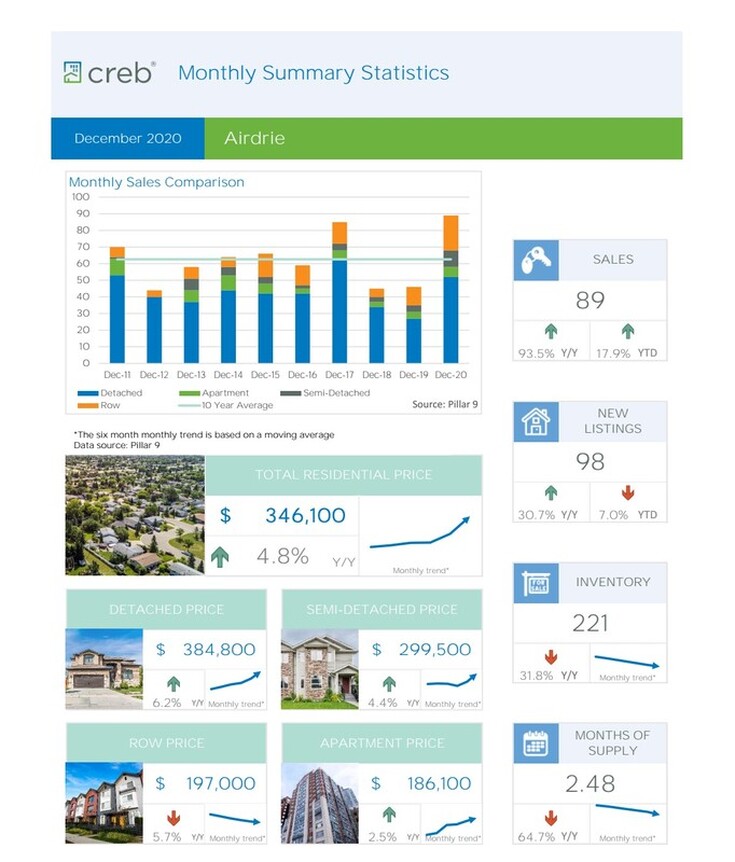

With December sales of 1,199, this is the highest December total since 2007. "Housing demand over the second-half of 2020 was far stronger than anticipated and nearly offset the initial impact caused by the shutdowns in spring. Even with the further restrictions imposed in December, it did not have the same negative impact on housing activity like we saw in the earlier part of the year," said CREB® chief economist Ann-Marie Lurie. Attractive interest rates along with prices that remain lower than several years ago have likely supported some of the recovery in the second half of the year. However, it is important to note that annual sales activity declined by one per cent compared to last year and remain well below long-term averages. New listings in December increased by 11 per cent. However, the number of sales exceeded the number of new listings in December contributing to further declines in inventory. Reductions in supply and improving demand in the second half of the year have contributed to some of the recent price improvements in the market. However, the recent gain in the benchmark price was not enough to offset earlier pullbacks as the annual residential benchmark price in Calgary declined by one per cent over last year. The pandemic has resulted in a significant shift in economic conditions, yet the housing market is entering 2021 in far more balanced conditions than we have seen in over five years. This will help provide some cushion for the market moving into 2021, but conditions will continue to vary depending on price range, location, and product type. More information about the 2021 housing market forecast for Calgary will be available at the CREB® Forecast on Tuesday, January 26, 2021. For more event details, please visit crebforecast.com. HOUSING MARKET FACTS Detached Stronger sales in the second half of the year were enough to offset earlier pullbacks as detached sales totalled 9,950, just slightly higher than last years' levels. Despite the modest gain, detached sales activity remains at the lower levels recorded since the stress test was introduced in 2018. Supply adjustments is causing sellers' market conditions for detached homes across all districts except the West and City Centre. This has helped support some price recovery in the market over the past several months. Annual city-wide price remains relatively flat compared to last year, but there were notable annual gains in both the South and South East districts which both recorded price gains of nearly two per cent. Despite some of the annual shifts seen, prices remain well below previous highs in all districts of the city. Semi-Detached Sales growth in the North East, North, West and South East district were offset by declines in the City Centre, North West, South and East districts. Sales this year of 1,663 were similar to levels recorded last year. While sales did not improve across each district, there were reductions in supply across all districts and is helping to reduce the months of supply. These reductions are starting to impact prices, but it was not enough to offset earlier pullbacks. City wide semi-detached prices eased by over one per cent in 2020, with the largest declines occurring in the City Centre, North West and West areas. Row Slower sales in the west district were not enough to offset the gains recorded in the rest of the city. Row sales totalled 2,145 in 2020, nearly two per cent higher than last years' levels. Despite the gains, levels continue to remain below long-term averages for the city. Rising sales were generally met with a reduction in supply. This is causing the months of supply to trend down, especially over the second half of the year. The decline in the months of supply was enough to help support some stability in prices. However, the adjustment did not occur soon enough and annual prices eased by nearly two per cent compared to the previous year and remain nearly 14 per cent below previous highs. Price adjustments did vary depending on location. The steepest decline occurred in the North East with a year-over-year decline of five per cent. The strongest gain occurred in the West district with a two per cent rise. Apartment Condominium Sales this month were the best December since 2014. However, it was not enough to offset earlier pullbacks as apartment condominium sales eased by ten per cent in 2020. This is the slowest year for apartment condo sales since 2001 and the only property type to record a significant annual decline in sales. Unlike other property types, supply levels have not adjusted in the same way and this segment remains oversupplied. Prices have trended down over the past two months due to excess supply. On an annual basis, the benchmark price declined by over two per cent this year and is over 16 per cent below the highs set in 2015. REGIONAL MARKET FACTS Airdrie December sales reached a new record high for the month. Improving sales throughout the second half of the year contributed to the annual sales of 1,407, a year-over-year gain of 18 per cent. New listings also rose in December and is likely contributing to some of the monthly gains in sales. Overall, new listings have remained well below last year. Along with improving sales, this is causing inventories to decline. Months of supply has remained below three months since June and prices have trended up. By December, the benchmark price had risen by nearly five per cent compared to last year. On an annual basis, the gains in price were enough to offset the earlier pullbacks and is creating stability in prices. However, this was not the case for all product types. Detached prices rose by nearly two per cent on an annual basis. Benchmark prices for row and apartment style product eased by a respective seven and one per cent compared to last year. Cochrane Record sales in December contributed to the annual gain of 16 per cent, making it the best year of sales compared to the past five years. New listings in 2020 also eased compared to last year. Rising sales and less new listings on the market caused inventories to ease to the lowest levels recorded since 2014. With months of supply of only two months, prices continued to trend up. December benchmark price was $419,900 and is a 5 per cent gain over last year. Prices have trended up over that past six months but remain relatively stable compared to last year. This is due to easing prices for higher density products offsetting gains in the detached sector. Okotoks Despite further declines in new listings, December sales improved. Year-to-date sales increased by nearly eight per cent. The lack of new listings and stronger sales caused inventories to drop to 63 homes in December, the lowest level for any month seen since 2006. The lack of inventory and high demand has supported increasing prices for the second half of the year. As of December, the benchmark price was $434,700, nearly two per cent above last years' levels. Despite the recent gains, 2020 benchmark prices remain over one per cent below last years' levels. However, this could be due to steeper price declines for semi, row and apartment style product. Provided by CREB City of Calgary, November 1, 2020 –

With strong gains in the detached sector, October sales in the city reached 1,764 units. This is a 23 per cent increase over last year and well above longer-term averages. The gain in citywide residential sales outpaced the growth in new listings, supporting tighter market conditions and improving prices. “Over the past several years, higher lending rates and the stress test pushed many out of the detached housing market. However, recent declines in rates, combined with prices that are lower than several years ago, have brought back some of that demand,” said CREB® chief economist Ann-Marie Lurie. “This is helping support more balanced conditions and price improvements in the market. However, price improvements are not occurring across all product type and price ranges and downside risk still hangs over future conditions.” Improving sales over the past four months were not enough to offset the pullbacks in the second quarter, leaving year-to-date sales nearly six per cent below last year’s levels. The same is also true for prices. Benchmark prices have trended up over the past four months and October prices were slightly higher than 2019. On a year-to-date basis, prices are one per cent lower than last year’s levels and nearly 10 per cent below previous highs. HOUSING MARKET FACTS Detached Detached sales totalled 1,139 in October, a year-over-year gain of 35 per cent. Unlike earlier this year, October’s largest gains in sales occurred for homes priced above $600,000. Easing prices for more expensive homes could be supporting this rise in sales. There were more new listings this month than levels recorded last year, but inventories still eased, causing the months of supply to drop below three months. This is a significant improvement from the four-plus months recorded over the past several years. There is, however, significant variation by location and price range. Detached homes priced under $500,000 are reporting less than two months of supply, supporting some price gains depending on location. When looking at price movements by district, the only city district to record further price declines was the City Centre. The South and South East districts recorded year-over-year price gains of around four per cent. Despite recent price movements, prices in all districts remain far from recovery and are well below previous highs. Semi-Detached Sales activity trended up over the last month and new listings eased. This is causing inventories to decline and the months of supply to fall to just above three months. The tighter market conditions continued to support some monthly gains in prices. Despite these gains, the October benchmark price remained nearly one per cent below last year’s levels. However, activity varies significantly based on location. Year-over-year prices eased in the City Centre, North West and West districts, offsetting the price gains in the other districts. Despite improvements over the past several months, year-to-date sales remain over six per cent below last year’s levels and over seven per cent below long-term averages. Slower sales activity has been mostly driven by pullbacks in the City Centre, North West, South, West and East districts of the city. Row There were significant year-over-year declines in the City Centre and West districts, but citywide row sales improved over last year’s levels and year-to-date activity sits only two per cent below last year. Inventory remained relatively stable this month, keeping the months of supply around four months. Citywide benchmark prices were $274,400 in October. This is a slight improvement over last month, but nearly six per cent below last year’s levels. The price decline was mostly caused by the significant drop in row prices in the West district of the city. Apartment Condominium For the seventh consecutive month, apartment condominium sales eased compared to last year’s levels, resulting in year-to-date sales of 1,999 units. This represents a 15 per cent decline from last year and is nearly 30 per cent below longer-term averages. The only sector of this market showing signs of improvement is the under-$200,000 segment. Sales have improved in this segment, but it has not been enough to offset declines in all other price ranges. Citywide sales have been easing, but new listings have been on the rise. This is causing year-over-year inventory gains and is halting positive momentum in prices. As of October, the benchmark price totalled $248,600, similar to last month and over one per cent below last year’s levels. Overall, apartment condominium prices remain over 17 per cent below previous highs. Airdrie With significant gains in the detached sector, sales once again improved this month compared to last year. The increased activity contributed to the year-to-date sales of 1,199 units. This is a 13 per cent increase over last year’s levels. The year-over-year gain in new listings was not enough to outpace the sales gains. As a result, inventories continue to trend down compared to the previous month and remain well below last year’s levels. This caused the months of supply to remain just above two months. Citywide year-to-date benchmark prices remained relatively stable compared to last year. However, activity does vary by product type. Detached year-to-date benchmark prices have increased by one per cent, while prices in all the other sectors remain below the previous year’s levels. Cochrane Sales activity this month rose compared to last year’s levels, contributing to a year-to-date increase of nearly ten per cent. Meanwhile, new listings have not kept pace with sales, causing reductions in inventory and the months of supply, which dropped to three months. Tighter housing market conditions are supporting price gains. Benchmark prices trended up for the fourth consecutive month and, as of October, were over two per cent higher than last year’s levels. Despite the recent gains, year-to-date prices remain one per cent below last year’s levels. Okotoks Improving sales in October were enough to push year-to-date sales up by one per cent. However, new listings contracted by a significant amount, causing inventory levels to ease and the months of supply to fall below two months. Persistent tightness in this market is supporting further monthly gains in prices. After five consecutive months of rising prices, October benchmark prices rose above last year’s levels. However, price gains have been driven by improvements in the detached market. Information provided by CREB Media release: Sales decline by two per cent from last year amidst COVID-19 pandemic

City of Calgary, July 2, 2020 – After three months where COVID-19 weighed heavily on the housing market, sales activity in June continued to trend up from the previous month, totalling 1,747 units. Caution remains necessary, as monthly sales are nearly two per cent lower than activity recorded last year. However, this represents a significant improvement compared to the past several months, where year-over-year declines exceeded 40 per cent. “Recent price declines, easing mortgage rates and early easing of social restrictions are likely contributing to the better-than-expected sales this month,” said CREB® chief economist Ann-Marie Lurie. “However, the market remains far from normal. Challenges, such as double-digit unemployment rates, will continue to weigh on the market for months to come.” New listings in June totalled 3,335 units, a six per cent increase over last year. The recent rise in new listings caused inventories to trend up, but they remain well below last year’s levels. Despite some recent monthly gains in supply, sales activity was high enough to cause the months of supply to dip below four months for the first time since May 2019. If this trend continues, it should help to ease the downward pressure on prices. Residential benchmark prices are comparable to last month, but they remain nearly three per cent lower than last year’s levels. HOUSING MARKET FACTS Detached

REGIONAL MARKET FACTS Airdrie

Media release: COVID-19's impact on Calgary housing market continues

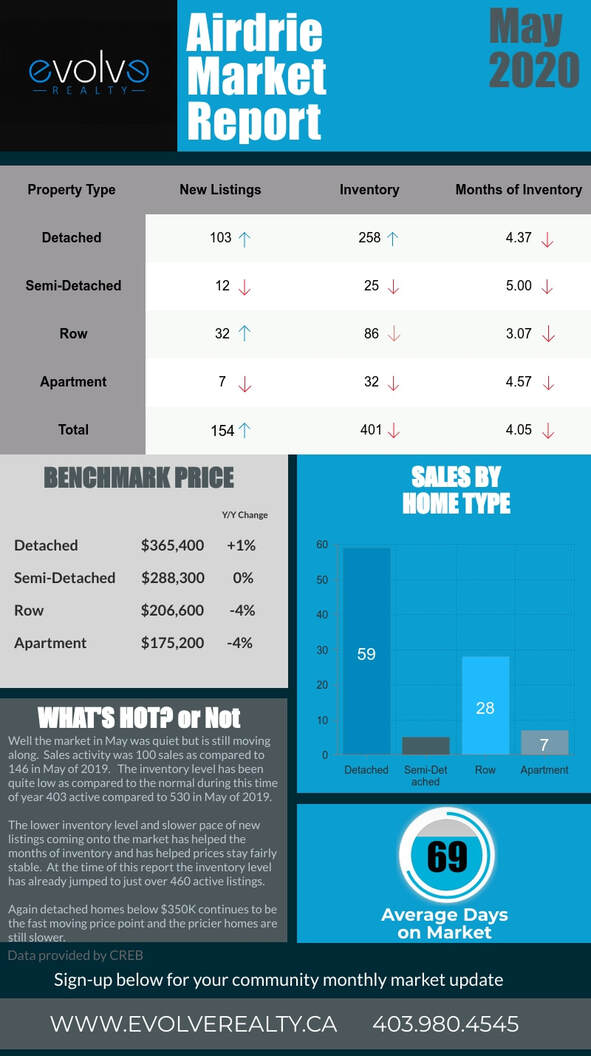

City of Calgary, June 1, 2020 – Housing market activity in May remained slow, but sales exceeded the lows from April, which saw less than 600 sales in Calgary. May sales totalled 1,080 units, a 44 per cent decline from last year's figures. "The initial shock of COVID-19 and social distancing measure is starting to ease. This is bringing some buyers and sellers back to the market. However, this market continues to remain far from normal and prices are trending down," said CREB® chief economist Ann-Marie Lurie. "Activity has also shifted toward more affordable product, which is likely causing differing trends depending on product type and price range." Sales are down in all price ranges, but a greater share of sales are priced below $500,000. In the higher price ranges the drop in inventory has not been enough compared to the drop in sales. Additionally, the months of supply is far higher than the already elevated levels seen during the past five years. The shift in sales toward lower-priced product is contributing to steep average price declines in the Calgary market. Benchmark pricing, which reflects comparisons of the same type of home, has eased by over two per cent compared to last year and 0.4 per cent compared to last month. This does not come as a surprise as the market continues to struggle with more supply than demand. COVID-19 and social distancing measures have contributed to rising unemployment rates and job losses throughout many economic sectors. This is weighing on consumer confidence and the housing market. Some of this job loss is temporary, but the energy sector remains the largest concern. Significant job loss throughout the typically higher-paid professional and technical services sector points to a longer adjustment period in the housing market, particularly in the higher end of the market. HOUSING MARKET FACTS Detached

REGIONAL MARKET FACTS Airdrie

Info provided by CREB City of Calgary, May 1, 2020 –

After the first full month with social distancing measures in place, the housing market is adjusting to the effects of COVID-19. April sales hit 573 units, a decline of 63 per cent over last year. "The decline in home sales does not come as a surprise. The combined impact of COVID-19 and the situation in the energy sector is causing housing demand to fall," said CREB® chief economist Ann-Marie Lurie. "Demand is also falling faster than supply. This is keeping the market in buyers' territory and weighing on prices." Sales activity eased across all price ranges, but the largest declines were for homes priced above $600,000. With a greater share of the sales occurring in the lower price ranges, the average price decline was more than eight per cent. Prices for the average home are also declining, reflected by the benchmark price, which fell by nearly two per cent compared to last year. New listings this month totalled 1,425 units, a decline of 54 per cent compared to last year. Inventories also declined, but with 5,565 units available, they remained high enough to push the months of supply above nine months. The economic impact of the situation is significant and early indications point toward more job losses and higher unemployment rates. Several government incentives will help cushion the blow, but challenges in the housing market are expected to persist throughout this year. HOUSING MARKET FACTS Detached

REGIONAL MARKET FACTS Airdrie

Info provided by CREB |

Evolve's BlogA place for us to share market news and information and chat about real estate related topics Archives

February 2021

Categories |

RSS Feed

RSS Feed

|

The trademarks REALTOR®, MLS®, Multiple Listing Service® and the associated logos are owned by The Canadian Real Estate Association (CREA) and identify the quality of services provided by real estate professionals who are members of CREA. Used under license Data supplied by CREB® MLS® System. CREB® is the owner of the copyright in its MLS® System. The Listing data is deemed reliable but is not guaranteed accurate by CREB®.

Copyright © 2014 Evolve Realty Inc. All Rights Reserved. |